Executive summary

2025 yılında sürdürülebilirlik paradoksal yeni bir aşamaya girdi: Temiz enerji ve geçiş yatırımları rekor seviyelere ulaşırken , fosil yakıt kaynaklı CO₂ emisyonları da yeni bir rekor kırdı . Küresel fosil yakıt ve çimento CO₂ emisyonlarının 2025 yılında yaklaşık %1,1 artarak 38,1 GtCO₂’ye ulaşması öngörülürken , 1,5°C hedefi için kalan karbon bütçesi yaklaşık 170 GtCO₂ olarak değerlendirildi; bu da 2025 emisyon seviyelerinde yaklaşık dört yıla denk geliyor.

On the governance side, COP30 in Belém shifted the multilateral conversation toward implementation and measurability, including a decision framework that calls for tripling adaptation finance by 2035, and supports tracking progress under the Global Goal on Adaptation through 59 voluntary indicators and related technical work. Meanwhile, the UNFCCC’s updated 2025 NDC synthesis found that, based on 86 NDCs submitted by 113 Parties, total 2035 global GHG emissions (with LULUCF) are projected to be around 12% below 2019 levels, and the updated NDCs represent about 69% of 2019 global emissions—progress, but still far from the pace required for 1.5°C pathways.

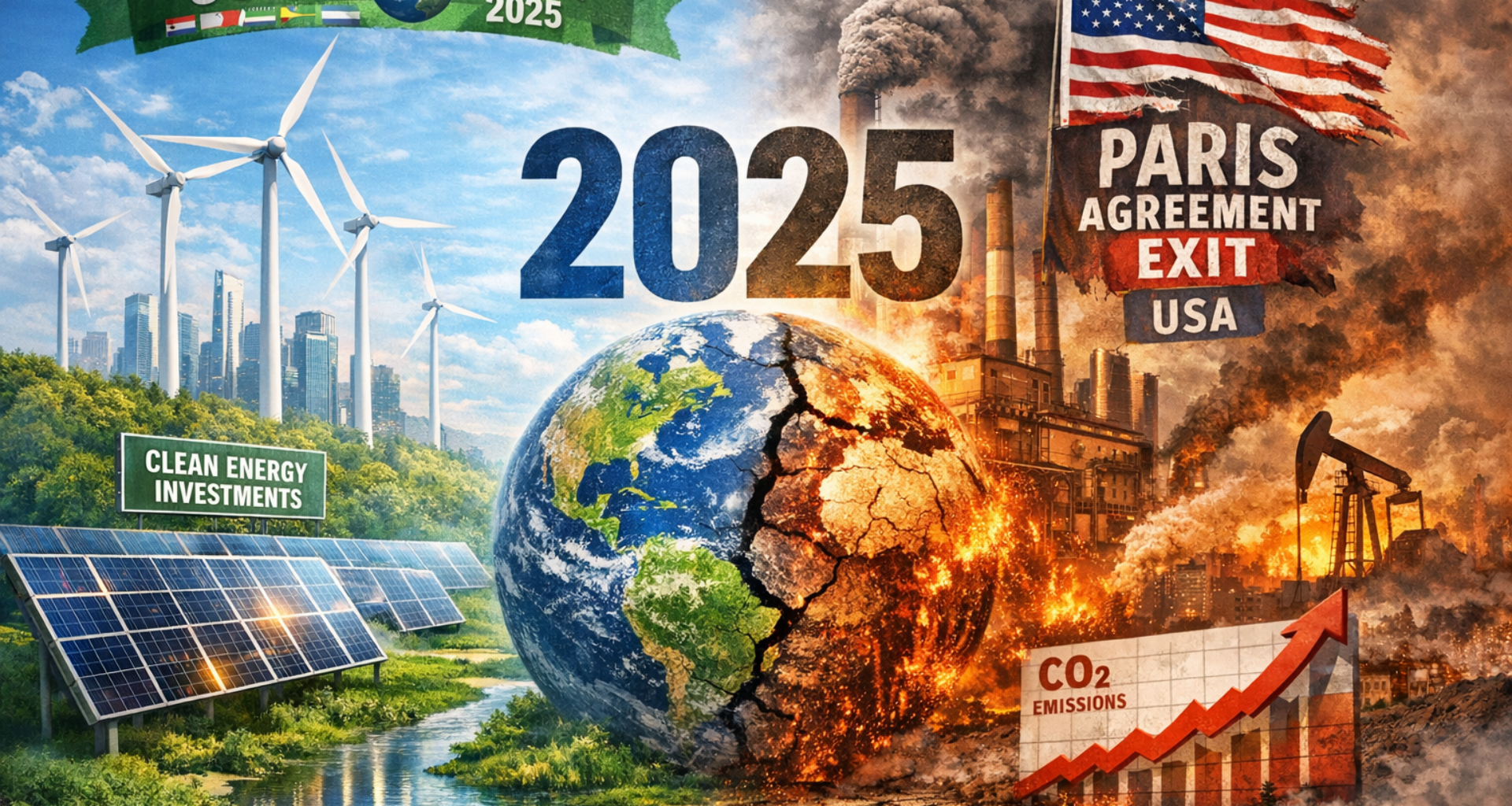

2025 also marked a sharper “Paris dynamics” shock: the United States’ withdrawal from the Paris Agreement was effected on 27 January 2025 and is scheduled to take effect on 27 January 2026, by UN depositary notification. At the same time, biodiversity governance achieved a milestone: the BBNJ “High Seas” treaty reached the 60-ratification threshold on 19 September 2025, triggering entry into force 120 days later (17 January 2026). By contrast, global negotiations for a binding plastics treaty (INC-5.2, Geneva) ended in August 2025 without agreement, underscoring the difficulty of aligning production-side and waste-side approaches.

At the sector and technology level, 2025 was a scale year. Global energy investment was set to reach USD 3.3 trillion, including USD 2.2 trillion in “clean” areas (renewables, nuclear, grids, storage, low-emissions fuels, efficiency, electrification). Electric car sales were expected to exceed 20 million in 2025—about one-quarter of global car sales. Batteries moved from “enabling tech” to “system cornerstone”: the global lithium-ion battery market exceeded USD 150 billion in 2025.

Finally, accountability tightened through disclosure and litigation. The first companies subject to the EU’s CSRD applied the new rules for FY 2024, with reports published in 2025, while the Commission also delivered a targeted ESRS “quick fix” to reduce certain disclosure burdens in FY 2025–2026. Globally, climate litigation continued to accelerate: by 30 June 2025, there were 3,099 climate-related cases filed across 55 national jurisdictions and 24 international/regional forums.

2025 snapshot

2025 can be captured in a handful of “anchor facts” that editors can reuse as a framing device:

- Emissions reality: fossil fuel and cement CO₂ emissions hit 38.1 GtCO₂ (record), and the 1.5°C carbon budget was estimated at 170 GtCO₂ (about four years at current levels).

- Clean investment reality: global energy investment rose toward USD 3.3T, with USD 2.2T going to clean energy technologies and enabling infrastructure.

- Mobility turning point: global electric car sales were expected to exceed 20 million in 2025 (≈ 25% market share).

- Adaptation gap: developing-country adaptation finance needs were updated to USD 310–365B/year by 2035, while international public adaptation finance flows were USD 26B in 2023.

- Paris volatility: the US withdrawal from the Paris Agreement was effected 27 Jan 2025; it takes effect 27 Jan 2026.

- Nature and pollution: the High Seas treaty hit 60 ratifications on 19 Sep 2025 (entry into force 2026), while plastics treaty talks failed to conclude at INC-5.2 (Geneva, Aug 2025).

Global policy and agreements

COP30 in Belém: implementation, adaptation finance, and measurable resilience

COP30 in Belém culminated in the Belém Package, a set of decisions that—among other elements—calls for tripling adaptation finance by 2035 and anchors follow-on work through the Baku Adaptation Roadmap (2026–2028).

The policy significance is less about inventing a new goal than making adaptation trackable: Parties agreed to operationalize progress measurement under the Global Goal on Adaptation through 59 voluntary indicators (“Belém Adaptation Indicators”) and related methodological work under the framework for global climate resilience.

Editorially, COP30’s adaptation outcome is best described as a shift from “principles” to “instruments”: financing ambition (tripling by 2035) paired with a measurement scaffold (indicators and review processes) designed to reduce the “adaptation opacity problem”—where money is pledged but outcomes remain hard to compare across countries and sectors.

NDCs and the Paris cycle: incremental improvements in pledges, insufficient pace for 1.5°C

The UNFCCC’s 10 November 2025 update to the NDC synthesis found that, based on 86 NDCs submitted by 113 Parties, total global GHG emissions in 2035 are projected to be around 12% below 2019 levels (with LULUCF). These updated NDCs represent about 69% of 2019 global emissions, meaning the majority—but not all—of emissions are covered by submitted plans, and a large “implementation gap” remains.

This matters because UNEP’s assessment of the emissions gap indicates that by 2035, emissions reductions of 35% (2°C pathway) and 55% (1.5°C pathway) relative to 2019 would be needed—far beyond what current NDC trajectories imply.

A notable counterpoint within the Paris cycle is that some jurisdictions used 2025 to sharpen mid-term trajectories. For example, the EU submitted an updated NDC in November 2025 reiterating its 2030 target and introducing an indicative 2035 target, signaling an attempt to extend policy continuity beyond 2030.

Paris dynamics and geopolitical volatility: the US withdrawal timeline

A defining “Paris dynamics” development was the formal US withdrawal path. The UN depositary notification states that the withdrawal action was effected on 27 January 2025 and will take effect for the United States on 27 January 2026, in line with Article 28 of the Agreement. The White House executive order issued 20 January 2025 directed immediate submission of the withdrawal notification to the UN Secretary-General as depositary.

The editorial takeaway is straightforward: 2025 hardened the sense that Paris implementation will proceed through uneven coalitions and sub-global alignment, rather than uniform superpower consensus—raising the value of standards, markets, and supply-chain rules that can persist across electoral cycles.

High Seas Treaty milestone and plastics treaty stalemate: progress on biodiversity, friction on production

In September 2025, the BBNJ Agreement reached the 60-ratification threshold (19 September 2025), positioning it to enter into force 120 days later.

In contrast, negotiations to finalize a global, legally binding plastics instrument stalled. INC-5.2 was held in Geneva from 5–15 August 2025, and official session documentation and reporting confirm that Parties did not reach consensus on the text—reflecting persistent divergence on definitions, scope, production controls, and financing mechanisms.

Suggested images (placeholders)

Image 1 (16:9): COP30 Belém conference scene

Alt text: “Delegates at COP30 in Belém discussing climate implementation and adaptation finance.”

Image 2 (16:9): High Seas Treaty / ocean conservation illustration

Alt text: “Concept image of biodiversity protection in areas beyond national jurisdiction (High Seas Treaty).”

Image 3 (16:9): Plastic pollution negotiations / Geneva conference

Alt text: “International negotiations on a global plastics treaty in Geneva.”

Image 4 (16:9): Marine protected area concept

Alt text: “High seas marine protected area concept visualization.”

Major international reports and signals

Carbon arithmetic: record emissions, shrinking carbon budget

The 2025 Global Carbon Budget communication projected fossil fuel and cement CO₂ emissions at 38.1 GtCO₂ in 2025 (≈ +1.1% year-on-year). It assessed the remaining carbon budget for 1.5°C at about 170 GtCO₂, equivalent to roughly four years at 2025 emissions levels; it also projected atmospheric CO₂ concentration reaching 425.7 ppm in 2025.

These numbers are editorially powerful because they translate sustainability from “target setting” into time-bounded scarcity: the budget framing turns “1.5°C” into a near-term resource constraint rather than a distant aspiration.

UNEP’s gap framing: the emissions gap and the adaptation gap

UNEP’s Emissions Gap Report 2025 (Off Target) concludes that, in 2035, reductions of 35% and 55% compared with 2019 levels would be needed for 2°C- and 1.5°C-aligned pathways, respectively, and warns that a higher exceedance of 1.5°C is very likely within the next decade given current momentum.

UNEP’s Adaptation Gap Report 2025 updates developing-country adaptation finance needs to USD 310B/year in 2035 (modelled costs), rising to USD 365B/year when extrapolated from expressed needs in NDCs/NAPs; it reports international public adaptation finance flows to developing countries at USD 26B in 2023, down from USD 28B the year prior.

Together, these reports reposition “adaptation” from a secondary pillar to a capital-allocation and risk-management problem—one increasingly relevant to infrastructure, insurance, sovereign credit risk, and supply-chain continuity.

IEA’s system lens: investment scale, EV adoption, methane transparency, and electricity security

The International Energy Agency projected global energy investment at USD 3.3T in 2025, with USD 2.2T going to clean energy technologies and enabling areas—about twice what goes to oil, gas, and coal (USD 1.1T). The IEA also highlights that grid investment—around USD 400B/year—risks lagging the pace of electrification and generation additions, creating an infrastructure bottleneck.

In mobility, IEA’s Global EV Outlook 2025 states that electric car sales exceeded 17M in 2024 (over 20% share) and were expected to exceed 20M in 2025 (about one-quarter of global car sales).

In methane, the IEA’s Global Methane Tracker 2025 emphasizes the growing role of satellites and measurement campaigns and adds new elements such as country-level historical emissions data and estimates from abandoned fossil fuel facilities. Its key findings note that more than 25 satellites can provide insights on methane emissions, strengthening 2025’s MRV ecosystem.

Finally, IEA’s World Energy Outlook 2025 underscores electricity’s expanding role and projects global electricity demand rising around 40% by 2035 in its stated policies scenario set, reinforcing why grid build-out and storage are now central to transition credibility.

WMO and IPCC: climate signal continuity and AR7 scaffolding

The World Meteorological Organization confirmed 2025 as one of the warmest years on record, with consolidated analysis placing global average surface temperature about 1.44°C ± 0.13°C above the 1850–1900 baseline; multiple datasets ranked 2025 as the second or third warmest year in a 176-year record.

On the science architecture side, the Intergovernmental Panel on Climate Change agreed in February 2025 (its 62nd Plenary Session in Hangzhou) on the outlines of the three Working Group contributions to the Seventh Assessment Report (AR7), formalizing the next cycle’s core assessment structure.

Country and regional policy moves

Across key jurisdictions, 2025 emphasized market creation (ETS/carbon credits), disclosure enforcement, and sector mandates. The unifying theme was not “new targets,” but new operating systems for targets: cap-and-trade expansion, performance standards, reporting baselines, and sector fuel rules.

Selected policy moves table

| Region / jurisdiction | 2025 action | Expected impact on sustainability outcomes | Editorial note |

|---|---|---|---|

| United States | UN depositary confirms withdrawal effected 27 Jan 2025, effective 27 Jan 2026 | Introduces volatility into the Paris political landscape and can slow global momentum depending on spillovers | Timeline is officially documented by UN depositary; policy shocks matter as much as targets |

| China | Expansion of national ETS to steel, cement, aluminium; ~1,500 enterprises added; first compliance deadline end-2025 | Extends carbon pricing signal to heavy industry; creates incentives for efficiency and technology shifts | Coverage rises toward ~8B tons, >60% of China’s CO₂ emissions (reported) |

| India | Carbon Credit Trading System (CCTS) advances via emissions-intensity target design for FY 2025–26 and 2026–27 | Builds market infrastructure for industrial decarbonization and compliance credits | Targets described as phased and increasingly stringent across periods |

| Türkiye | First Climate Law adopted (July 2025) establishing legal basis for national ETS; ETS draft regulation published July 2025 | Creates legal and procedural foundation for carbon pricing and MRV integration | Official announcements confirm legislative adoption and draft ETS regulation publication |

| European Union | CSRD/ESRS first application for FY 2024 with reports in 2025; Commission adopts ESRS “quick fix” (FY 2025–26 relief for certain disclosures) | Embeds sustainability disclosure into audited reporting and capital markets; reduces some “first-wave” friction | The politics of “simplification” becomes a 2025 storyline—important for editors to track |

| European Union (transport fuels) | ReFuelEU Aviation: SAF supply mandate begins in 2025; FuelEU Maritime applies from 1 Jan 2025 | Creates demand-pull for SAF and low-GHG maritime fuels; pressures fuel supply chains | SAF mandates also trigger supply concerns and debate on realism |

Sector innovations and scaled solutions

Energy and grids: investment scale meets the “grid bottleneck”

2025’s energy transition story starts with money, but ends with infrastructure. Global energy investment rising to USD 3.3T and clean investment to USD 2.2T signals that capital now broadly accepts the transition direction. Yet the warning that grid investment remains around USD 400B/year frames a practical constraint: without faster permitting, interconnection, and system upgrades, clean generation can become “stranded” behind bottlenecks.

Storage helps relieve this, but it is not frictionless. Batteries also reached a different kind of milestone: the global lithium-ion battery market exceeded USD 150B in 2025, underlining the sector’s economic (and geopolitical) weight.

Transport: EV maturation, and the hard reality of SAF supply

Electric vehicles were the clearest mass-market scaling signal in 2025. Electric car sales exceeded 17M in 2024 and were expected to exceed 20M in 2025, reaching roughly 25% of global car sales.

Aviation decarbonization, by contrast, was a “constraint story.” In the EU, the ReFuelEU Aviation framework sets a mandatory SAF supply mandate starting at 2% in 2025 (and rising thereafter). But industry reporting underscored a structural tension: targets are difficult given limited supply, and SAF was expected to account for only ~0.7% of global airline fuel consumption in 2025.

Agriculture, methane, and MRV: from invisible emissions to measurable liabilities

Methane is a near-term climate lever, and 2025’s progress was as much about visibility as abatement technology. Expanded satellite coverage and measurement-based datasets strengthen policymaker and investor capacity to attribute and prioritize emissions sources. With 25+ satellites contributing methane insights, the MRV ecosystem increasingly supports enforcement-oriented approaches rather than only voluntary reporting.

Construction and heavy industry: credible pathways require hydrogen, CCUS, and procurement signals

Heavy industry remains the transition’s “hard core.” In steel, a notable 2025 development was BHP and POSCO’s agreement to advance “near-zero emissions” ironmaking using POSCO’s hydrogen-based technology (HyREX), combining hydrogen reduction and an electric smelting furnace.

In cement and concrete, progress reporting emphasizes CCUS as essential and highlights a milestone: a first net-zero commercial-scale cement plant using carbon capture and storage entered operation—framing CCUS as technically demonstrated but dependent on policy support and project pipelines for scale.

Circular economy: “recycling” is not enough; product rules and global coordination matter

The Circularity Gap Report 2025 found that the global circularity rate fell to 6.9%, indicating that only 6.9% of materials entering the global economy are secondary—despite improvements in some recycling metrics—because overall material consumption continues to grow.

In Europe, 2025 strengthened the regulatory toolkit for circularity: the Packaging and Packaging Waste Regulation (PPWR) entered into force on 11 February 2025, aiming to reduce packaging waste and foster circular product systems. The Commission also adopted the first ESPR and Energy Labelling Working Plan in April 2025, signaling a push toward product-level rules that can shape upstream material choices and design standards.

Finance, standards, and accountability

Finance and carbon pricing: record flows, uneven distribution, and market-design challenges

BloombergNEF reported global investment into the energy transition at USD 2.3T in 2025 (+8% vs 2024), led by electrified transport (USD 893B), renewable energy (USD 690B), and grid investment (USD 483B).

Climate Policy Initiative reported global climate finance reaching USD 1.9T in 2023, with private finance crossing USD 1T—a key signal that sustainability is increasingly financed through private capital channels, not only public budgets.

Carbon pricing expanded steadily. The World Bank’s State and Trends of Carbon Pricing 2025 reports that carbon pricing covers around 28% of global emissions and mobilized over USD 100B for public budgets in 2024; it also notes the pool of unretired carbon credits moved toward almost 1B tons in 2024 as supply continued to outstrip demand.

Disclosure and standards: converging baselines, political friction

In the EU, 2025 was the “go-live” year for the first CSRD cohort: first companies subject to CSRD must apply the rules for FY 2024, for reports published in 2025. The Commission also adopted a “quick fix” amendment (July 2025) allowing certain 2024 reporters to omit specific anticipated financial-effects disclosures for FY 2025 and FY 2026.

Implementation realities emerged quickly. Early monitoring found wide variability in sustainability statement length (triple-digit pages on average), highlighting that comparability is a work in progress even under a common standard.

At the global baseline level, the IFRS Foundation reported in June 2025 that 36 jurisdictions have adopted or used the IFRS Sustainability Disclosure Standards (ISSB Standards) or are finalising steps toward introduction.

Civil society, litigation, and enforcement: the rise of the courtroom and procedural accountability

UNEP’s Global Climate Litigation Report 2025 status review reports that by 30 June 2025, there were 3,099 climate-related cases across 55 national jurisdictions and 24 international or regional mechanisms.

Meanwhile, the plastics treaty negotiations highlight another civil-society dynamic: observers pressed for stronger provisions, while official and reporting sources document persistent disagreements on whether the treaty should address production limits and chemicals of concern versus focusing on waste management and design.

Key statistics and indicators table

| Indicator | 2025 value / projection | Why it matters | Primary source |

|---|---|---|---|

| Fossil fuel & cement CO₂ emissions | 38.1 GtCO₂ (record; projected +1.1%) | Shows the transition has not yet produced absolute global decline | Global Carbon Budget 2025 |

| Remaining 1.5°C carbon budget | 170 GtCO₂ (≈ four years at 2025 levels) | Translates 1.5°C into a near-term constraint | Global Carbon Budget 2025 |

| Atmospheric CO₂ concentration | 425.7 ppm (projected 2025) | Highlights continued atmospheric accumulation | Global Carbon Budget 2025 |

| Global energy investment | USD 3.3T (2025) | Benchmark for transition scale and energy security framing | IEA World Energy Investment 2025 |

| Clean energy investment | USD 2.2T (2025) | Clean areas attract ~2× fossil investment; signals structural shift | IEA World Energy Investment 2025 |

| Energy transition investment | USD 2.3T (2025) | Confirms record transition spending and where it concentrates | BloombergNEF ETIT 2025 |

| EV sales | >20M electric cars in 2025; ≈ 25% share | Marks mass adoption threshold influencing oil demand and grids | IEA Global EV Outlook 2025 |

| Global lithium-ion battery market | >USD 150B (2025) | Batteries become a macro-industry and grid asset, not just EV component | IEA commentary / reporting |

| Adaptation finance needs (developing countries) | USD 310–365B/year by 2035 | Quantifies adaptation “investability” gap | UNEP Adaptation Gap Report 2025 |

| Carbon pricing coverage and revenues | Coverage ~28%; >$100B mobilized (2024) | Shows carbon pricing is mainstreaming, but quality and coverage vary | World Bank State & Trends of Carbon Pricing 2025 |

Notable case studies and editorial guidance

Case study: durable carbon removal demand outruns supply

The carbon-removal market’s 2025 storyline combined corporate ambition and physical scarcity. Reporting highlighted that durable CDR purchases rose sharply, while less than 1 million tons of durable carbon removal credits had been issued to date (as cited in reporting). In parallel, a major contract backed a Louisiana project to remove 6.75 million metric tons of CO₂ over 15 years, described as the largest permanent carbon removal project to date at the time of announcement.

This “demand-supply inversion” is important because it marks a shift from net-zero slogans to procurement reality: if supply is constrained, prices rise and credibility tests harden; if supply scales, it creates a new industrial subsector with MRV and liability requirements.

Case study: Türkiye’s move from strategy to legal architecture

In July 2025, Türkiye adopted its first climate law, and official communications confirm publication of a draft ETS regulation in July 2025—turning the ETS roadmap into a concrete policy workflow rather than a concept. This provides a useful “model case” of how middle-income economies build transition infrastructure: legislation → MRV alignment → market rules → compliance cycles.

Case study: the ocean governance breakthrough and its limits

The BBNJ treaty reaching 60 ratifications in September 2025 is a rare example of multilateral environmental governance achieving a clear legal milestone in a polarized context. Effectiveness will depend on implementation capacity, financing, and participation breadth.

Chart recommendations for editors

- “Double-record” chart (emissions vs investment):

- Series A: Fossil fuel & cement CO₂ emissions (GtCO₂), 2024–2025 projection

- Series B: Global energy investment (USD, 2024–2025; total and clean)

- Sources: Global Carbon Budget 2025; IEA World Energy Investment 2025

- “NDC trajectory reality check” chart:

- Series: UNFCCC projected 2035 emissions vs 2019 baseline (% change) and coverage share of 2019 emissions

- Source: UNFCCC NDC synthesis update (10 Nov 2025)

- “Adaptation finance gap” chart (needs vs flows):

- Series A: Developing-country adaptation finance needs (310–365B/year by 2035)

- Series B: International public adaptation finance flows (26B in 2023)

- Source: UNEP Adaptation Gap Report 2025

- “EV scale curve” chart:

- Series: Global electric car sales (2024 actual; 2025 expected) and market share (%)

- Source: IEA Global EV Outlook 2025

- “Carbon pricing mainstreaming” chart:

- Series A: Share of global emissions covered by carbon pricing (%)

- Series B: Carbon pricing revenues mobilized (USD, 2024)

- Series C (optional): unretired credit pool (tons)

- Source: World Bank State and Trends of Carbon Pricing 2025

- “Circularity slipping backward” chart:

- Series: Global circularity rate (%) with 2025 value highlighted at 6.9%

- Source: Circularity Gap Report 2025

Timeline (optional – Mermaid)

If your WordPress theme supports Mermaid, you can keep this. If not, remove this block.

timeline

title Sustainability milestones in 2025 (selected)

2025-01-20 : US executive order directs Paris withdrawal notification

2025-01-27 : UN depositary: US Paris withdrawal effected (effective 2026-01-27)

2025-02 : IPCC agrees outlines for AR7 Working Group contributions (Hangzhou)

2025-03-26 : China announces ETS expansion to steel, cement, aluminium

2025-05-07 : IEA Global Methane Tracker 2025 updates measurement-based estimates

2025-05-14 : IEA Global EV Outlook 2025: >20M EV sales expected in 2025

2025-06-05 : IEA World Energy Investment 2025: global investment set at $3.3T

2025-07-02 : Türkiye adopts first Climate Law establishing legal basis for ETS

2025-07-22 : Türkiye publishes draft ETS regulation

2025-08-05 : Plastics treaty talks (INC-5.2) resume in Geneva; no agreement by Aug 15

2025-09-19 : BBNJ High Seas treaty reaches 60 ratifications (120-day countdown)

2025-10-29 : UNEP Adaptation Gap Report 2025: $310–365B/year needed by 2035

2025-11-04 : UNEP Emissions Gap Report 2025: 35%/55% cuts needed by 2035 (vs 2019)

2025-11-13 : Global Carbon Budget 2025: fossil CO2 emissions record; 1.5°C budget ~170 Gt

2025-11 : COP30 Belém Package adopted (calls to triple adaptation finance by 2035)

Sources (URLs)

Global policy and agreements

- COP30 Belém Package (22 Nov 2025): https://cop30.br/en/news-about-cop30/cop30-approves-belem-package1

- UNFCCC COP30/CMA decision text (PDF): https://unfccc.int/sites/default/files/resource/cma2025_L25_adv.pdf

- UNFCCC NDC synthesis update (10 Nov 2025, PDF): https://unfccc.int/sites/default/files/resource/message_to_parties_and_observers_ndc_synthesis_report_update.pdf

- EU Council press release on updated EU NDC (5 Nov 2025): https://www.consilium.europa.eu/en/press/press-releases/2025/11/05/paris-agreement-the-eu-submits-its-updated-ndc-with-an-indicative-target-for-2035-to-the-un-ahead-of-cop30/

- UNEP on BBNJ threshold (19 Sep 2025): https://www.unep.org/unep-and-bbnj

- EU Commission press corner on ocean treaty milestone (19 Sep 2025): https://ec.europa.eu/commission/presscorner/detail/da/ip_25_2151

- EU DG MARE news on entry into force (16 Jan 2026): https://oceans-and-fisheries.ec.europa.eu/news/high-seas-treaty-enters-force-milestone-ocean-conservation-2026-01-16_en

- UNEP INC plastics session page (INC-5.2): https://www.unep.org/inc-plastic-pollution/session-5.2

- IISD ENB summary (INC-5.2): https://enb.iisd.org/plastic-pollution-marine-environment-negotiating-committee-inc5.2-summary

Major reports and indicators

- Global Carbon Budget 2025: https://globalcarbonbudget.org/fossil-fuel-co2-emissions-hit-record-high-in-2025/

- UNEP Emissions Gap Report 2025: https://www.unep.org/resources/emissions-gap-report-2025

- UNEP Adaptation Gap Report 2025: https://www.unep.org/resources/adaptation-gap-report-2025

- IEA World Energy Investment 2025 (exec summary): https://www.iea.org/reports/world-energy-investment-2025/executive-summary

- IEA World Energy Outlook 2025: https://www.iea.org/reports/world-energy-outlook-2025/overview-and-key-findings

- IEA Global EV Outlook 2025 (trends): https://www.iea.org/reports/global-ev-outlook-2025/trends-in-electric-car-markets-2

- IEA Global Methane Tracker 2025: https://www.iea.org/reports/global-methane-tracker-2025/key-findings

- WMO on 2025 warmth: https://wmo.int/news/media-centre/wmo-confirms-2025-was-one-of-warmest-years-record

- IPCC AR7 page: https://www.ipcc.ch/assessment-report/ar7/

- IPCC AR7 outlines news (Mar 2025): https://www.ipcc.ch/2025/03/01/ipcc-agrees-outlines-of-three-key-contributions-to-ar7/

Country and regional policy sources

- China ETS expansion (Reuters, 26 Mar 2025): https://www.reuters.com/sustainability/china-expand-carbon-trading-market-steel-cement-aluminium-2025-03-26/

- ICAP on China ETS expansion: https://icapcarbonaction.com/en/news/china-officially-expands-national-ets-cement-steel-and-aluminum-sectors

- India CCTS brief (IETA, PDF): https://www.ieta.org/uploads/wp-content/Resources/Busines-briefs/2025/IETA_Business_Brief-India_July_final-one.pdf

- ICAP on India targets: https://icapcarbonaction.com/en/news/india-notifies-emission-intensity-targets-nine-sectors-under-carbon-credit-trading-scheme

- Türkiye Climate Law (Ministry): https://csb.gov.tr/haberler/turkiyenin-ilk-iklim-kanunu-tbmm-de-kabul-edildi-302036

- Türkiye ETS draft regulation: https://iklim.gov.tr/turkiye-emisyon-ticaret-sistemi-yonetmeligi-taslagi-yayimlandi-haber-4519

- EU Commission CSRD timeline: https://finance.ec.europa.eu/capital-markets-union-and-financial-markets/company-reporting-and-auditing/company-reporting/corporate-sustainability-reporting_en

- EU Commission ESRS quick fix: https://finance.ec.europa.eu/publications/commission-adopts-quick-fix-companies-already-conducting-corporate-sustainability-reporting_en

- UN depositary notification on US Paris withdrawal (PDF): https://treaties.un.org/doc/Publication/CN/2025/CN.71.2025-Eng.pdf

- White House executive order page (Jan 2025): https://www.whitehouse.gov/presidential-actions/2025/01/putting-america-first-in-international-environmental-agreements/

- ReFuelEU Aviation: https://transport.ec.europa.eu/transport-modes/air/environment/refueleu-aviation_en

- EASA SAF page: https://www.easa.europa.eu/en/domains/environment/eaer/sustainable-aviation-fuels

- FuelEU Maritime (EMSA): https://www.emsa.europa.eu/newsroom/latest-news/item/5385-fueleu-maritime-full-application-1-january-2025.html

Finance, standards, and accountability

- BloombergNEF ETIT 2025: https://about.bnef.com/insights/clean-energy/bloombergnef-finds-global-energy-transition-investment-reached-record-2-3-trillion-in-2025-up-8-from-2024/

- CPI Global Landscape of Climate Finance 2025 (PDF): https://www.climatepolicyinitiative.org/wp-content/uploads/2000/06/compressed_Global-Landscape-of-Climate-Finance-2025.pdf

- World Bank State and Trends of Carbon Pricing 2025: https://www.worldbank.org/en/publication/state-and-trends-of-carbon-pricing

- IFRS jurisdictional profiles (Jun 2025): https://www.ifrs.org/news-and-events/news/2025/06/ifrs-foundation-publishes-jurisdictional-profiles-issb-standards/

- IFRS Türkiye profile (PDF): https://www.ifrs.org/content/dam/ifrs/publications/sustainability-jurisdictions/pdf-profiles/turkiye-ifrs-profile.pdf

- EFRAG State of Play 2025 (PDF): https://www.efrag.org/sites/default/files/media/document/2025-07/EFRAG_State%20of%20Play%202025%20Report_0.pdf

- UNEP Climate Litigation Report 2025: https://www.unep.org/resources/report/global-climate-litigation-report-2025-status-review

Sector and case study sources

- Reuters on durable CDR supply crunch (Nov 2025): https://www.reuters.com/sustainability/cop/big-tech-led-demand-carbon-removal-credits-fuels-supply-crunch-2025-11-18/

- Reuters on Microsoft–AtmosClear deal (Apr 2025): https://www.reuters.com/sustainability/cop/microsoft-signs-large-carbon-removal-deal-backing-atmosclears-louisiana-project-2025-04-15/

- GCCA Progress Report 2025/26 (PDF): https://gccassociation.org/wp-content/uploads/2025/11/GCCA_ProgressReport_2025_AW_FINAL-1.pdf

- BHP–POSCO HyREX partnership (Oct 2025): https://www.bhp.com/news/media-centre/releases/2025/10/bhp-and-posco-partner-to-advance-hydrogen-based-ironmaking-technology

- Circularity Gap Report 2025: https://www.circularity-gap.world/2025

- Circularity update note: https://www.circularity-gap.world/updates-collection/global-circularity-rate-fell-to-6-9—despite-growing-recycling

- EU packaging waste page (PPWR): https://environment.ec.europa.eu/topics/waste-and-recycling/packaging-waste_en

- EU ESPR page: https://commission.europa.eu/energy-climate-change-environment/standards-tools-and-labels/products-labelling-rules-and-requirements/ecodesign-sustainable-products-regulation_en